Xerox - A possible hidden gem [Updated]

- Pavaki Capital

- May 3, 2022

- 6 min read

Updated: Jul 15, 2022

With enthusiasm, we wrote a glowing commentary about Xerox on March 28, 2022. The company released Q1 2022 results and the stock declined from about $20 to $17.5. We feel like we fell on our faces. After examining the results, we still feel that Xerox stock provides a margin of safety.

Q1 2022 comments

Headline news focused on a Net Loss of $56 million as reported in the Income Statement but Xerox generated $50 million as free cash flow, (Non-GAAP financial measures)*. Still, the company maintains in its presentation that it will generate “at least $400 million of cash flow for the full year, 2022”.

The management blames, “Supply constraints continued to inhibit our ability fulfill demand in Q1…”

The management seems too committed to cutting the cost; they report:

Project Own It is a multi-year program to simplify our operations and instill a culture of continuous improvement

Achieved ~$1.8B of gross cost savings since 2018

Targeting a 50% increase above our initial gross cost savings target of $300M for 2022

One quibble with the management: even though the management team has learned financial engineering at Carl Icahn's feet, how come they have not securitized their FITTLE finance assets; FITTLE, the new name for its equipment financing business, Xerox Financial Services (XFS).

On all investors' behalf, we hope and pray management keeps their word, “At our Investor Day, we presented a sum-of-the-parts analysis that provided a range of values for our stock of $32 to $58 per share.” In that case, rather than falling on our face, our face will be glowing; but we will not say that we told you Xerox is a hidden gem.

*Company defined Free Cash Flow: To better understand trends in our business, we believe that it is helpful to adjust operating cash flows by subtracting amounts related to capital expenditures. Management believes this measure gives investors an additional perspective on cash flow from operating activities in excess of amounts required for reinvestment. It provides a measure of our ability to fund acquisitions, dividends and share repurchase.

For your convenience, we provide you with our previous article with the revised numbers for Q1 2022.

Xerox - A possible hidden gem

Short sellers evaluate companies including their financial statements, business models, management, and other items, forensically. Why? They want to reap a big profit by shorting the stock. Examples of fraud include Enron, WorldCom, Wirecard, and numerous other companies.

How about we evaluate a company to discover the hidden value? Both present and future value. To find a gem, we don’t have to chase hot soaring stocks.

How about ancient Xerox (XRX)? Xerox has survived so many ups and downs and can flourish again, in our opinion.

A stable ship

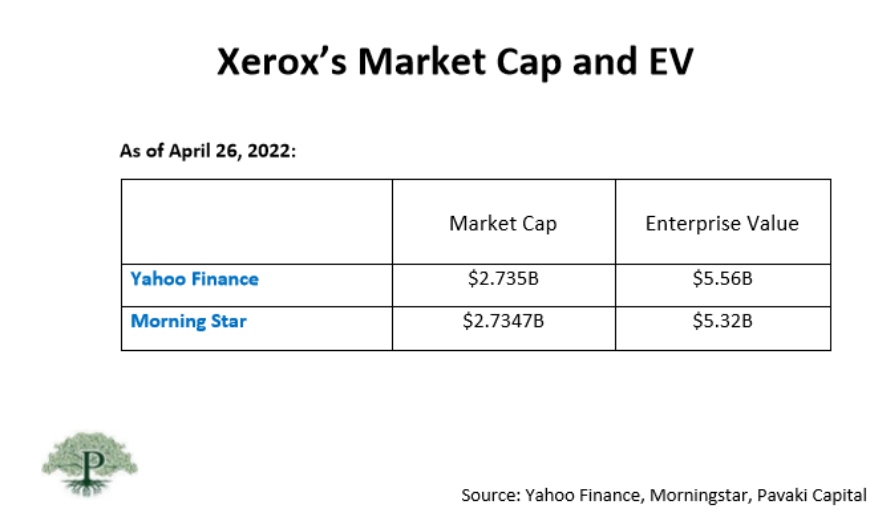

What are the Xerox market cap and enterprise value? We chose two popular financial sites to find the values.

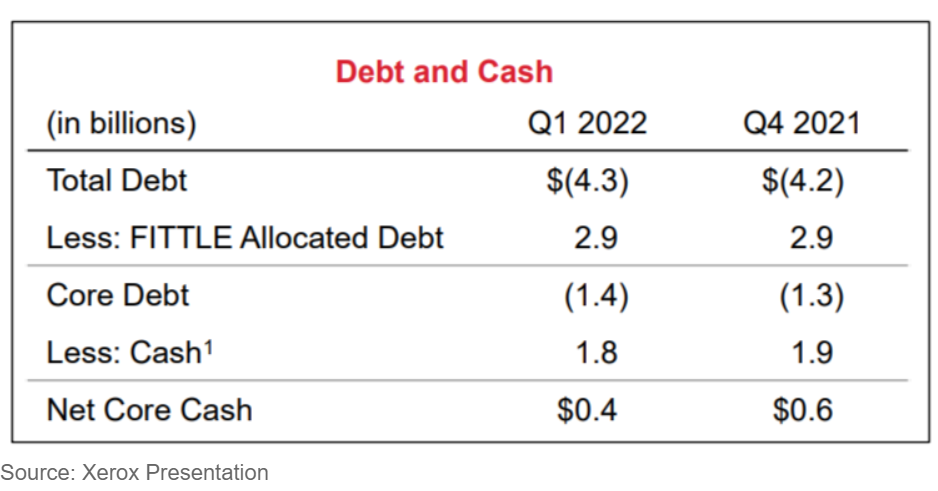

Xerox's almost double enterprise value than the market cap implies Xerox owes a sizable debt. Here is one of the slides from Xerox’s presentation:

As per the above slide:

Total debt = $4.3 billion

Cash and cash equivalent = $1.8 billion

Net Debt = $4.3 billion - $1.8 billion = $2.5 billion

But when we examine the balance sheet critically, we find one entry - $2.9 billion of finance receivables.

So, now Xerox does not owe the money but has net cash.

Net Debt = $2.5 billion

Financial receivable = $2.9 billion

Net Cash = $2.9 billion - $2.5 billion = $0.4 billion

We believe the company’s enterprise value shall be reported as:

$2.73 billion - $0.4 billion = $2.33 billion.

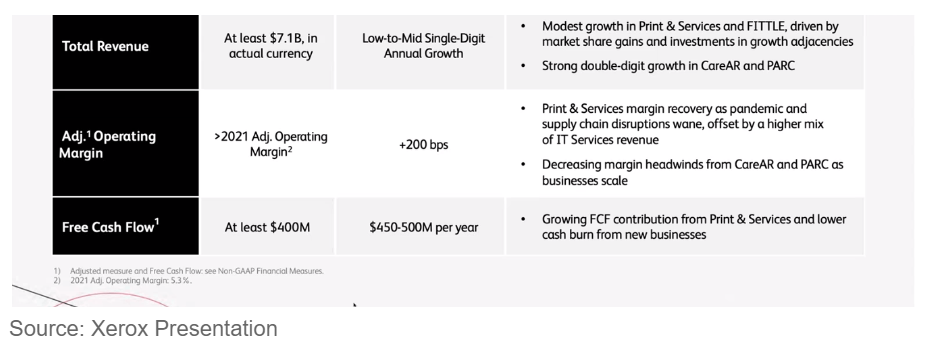

A company worth $2.33 billion will generate free cash flow of about $400 million in 2022. So, currently, Xerox is trading approximately six times its 2022 free cash flow.

How many companies trade less than six times free cash flow? Many hot and rising stocks have negative or zero cash flow.

Xerox tells us in its presentation that by 2023-24, it expects a free cash flow of $450-$500 million per year.

See below:

Upcoming businesses

1. We know Xerox's unsexy Print and Services business which is declining.

2. FITTLE finances the equipment it sells. The company may start financing other companies' sale of equipment also. If Xerox does not make mistakes, equipment financing can generate a solid return on employed capital.

Before the Q1 2022 results, Xerox had only securitized $0.56 billion out of $2.9 billion of FITTLE’s debt. For $2.9 billion - $0.56 billion = $2.3 billion, Xerox was liable, even though $2.9 billion is secured by the receivables. If the recession decreases collection of accounts receivables, Xerox will sustain the loss; currently FITTLE is not contributing towards the free cash flows. In other words, FITTLE can cause loss but does not add free cash flows at this time.

Incidentally, we, naive about corporate finance, don't understand why Xerox has not securitized the whole $2.9 billion FITTLE’s debt. Xerox management employs experts in financial engineering; the large shareholder Carl Icahn himself knows the finer point of passing the risk to others, by securitizing debt.

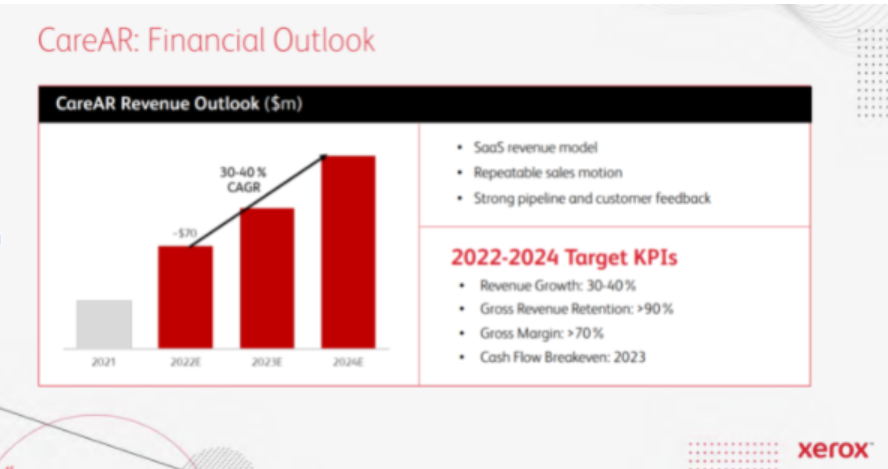

3. Xerox bought CareAR, which uses subscriptions to deliver an augmented (reality) customer experience. With labor shortages, the CareAR business can substantially grow.

Source: Xerox Presentation

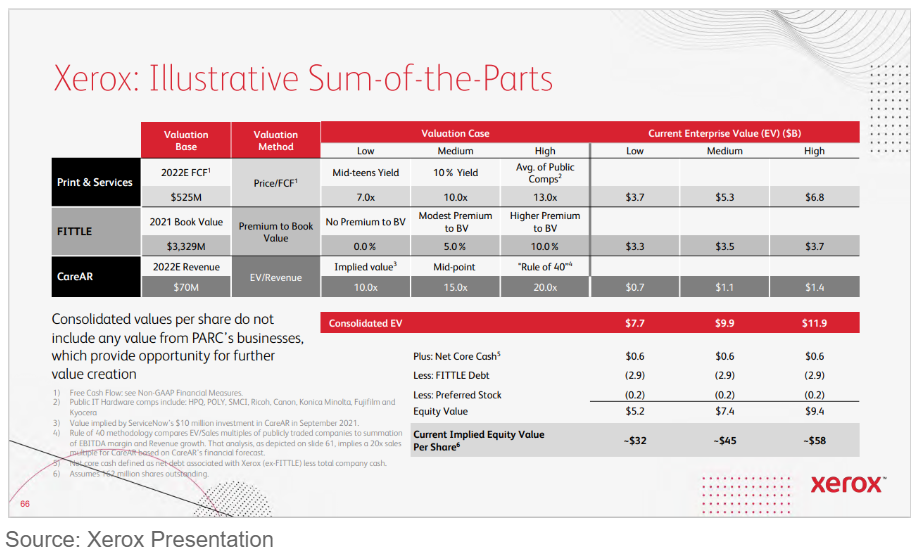

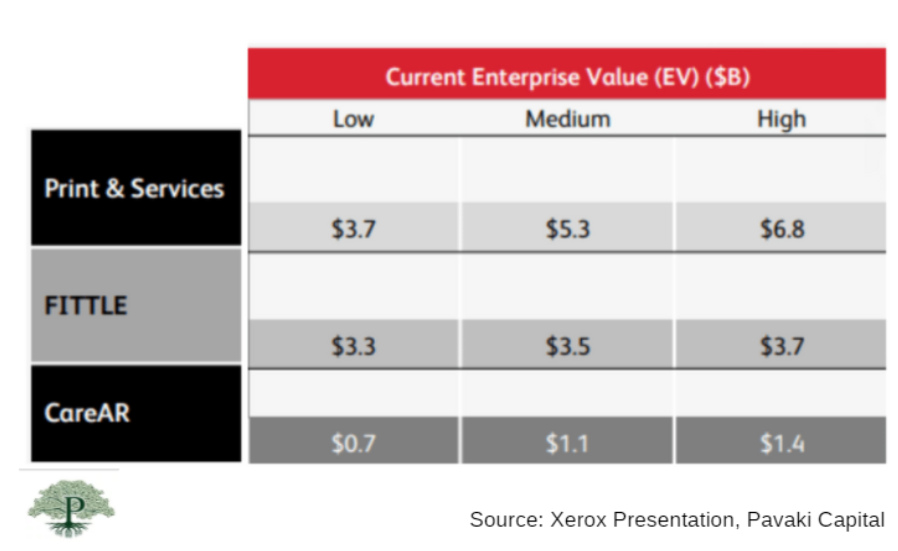

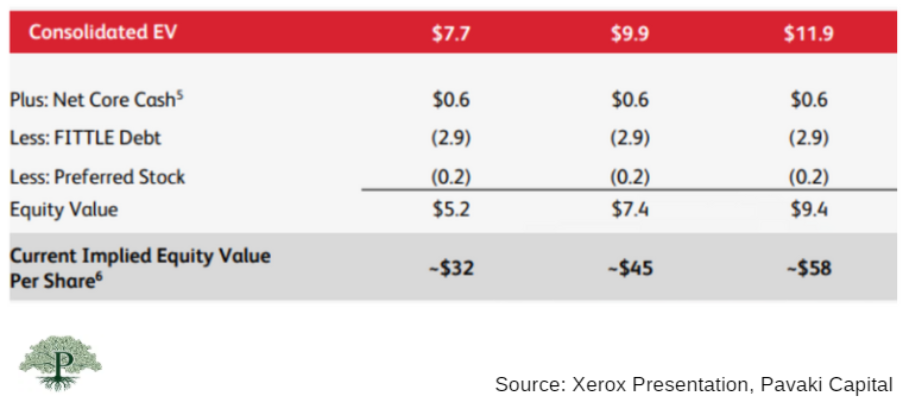

The company has projected the valuation of three businesses as follows:

For clarity, we reformatted the slide as follows:

The above projections implies Xerox equity value from anywhere $32 - $58. Compare the projected share price to the current share price of $17.66. I will be delighted if the projections come true of $32; that’s a gain of over 80%. While I am awaiting a potential 80% gain, I will collect a 5.6% yield. Which bank or the financial company returns 5% on the invested money?

Cloud Nine

Xerox is acting like a start-up. If one of the following business units takes off, Xerox's stock price can substantially increase.

In the past, unfortunately, Xerox has not monetized its innovations. We wish them the best this time.

Management

Carl Icahn has chosen the management team. Naturally, the successful investor does not want to lose his money. The management team seems experienced and shareholder friendly.

Time will tell.

Competition

Print and Services business faces tough competition from Brother Industries Ltd (BRTHY), Lexmark International Inc (LXK), Canon Inc (CAJ), HP Inc (HPQ), and other companies. So many companies engage in equipment financing. Competitors to CareAR will spring up.

Limitations of our analysis

We interpreted net cash on the Xerox balance sheet differently than most analysts. Are we right in our interpretation? You decide for yourself.

The businesses of FITTLE and CareAR may not take off

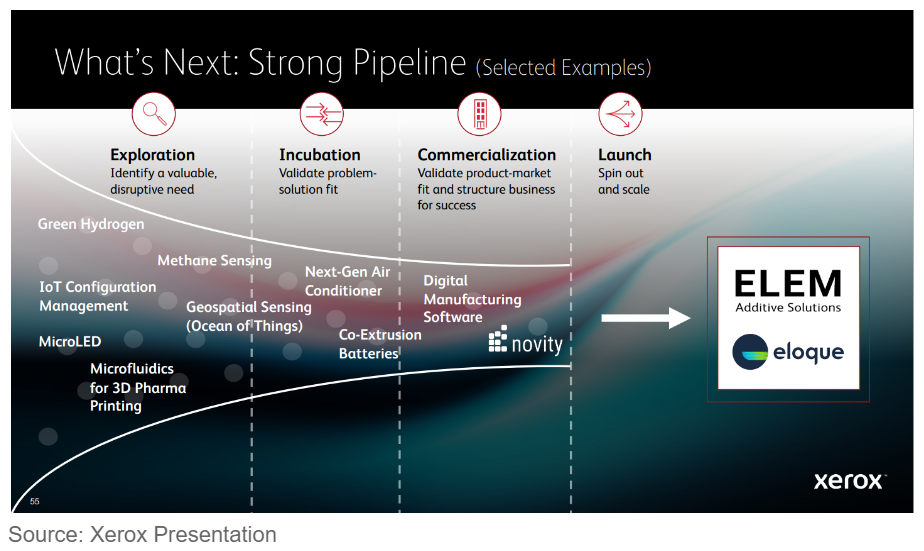

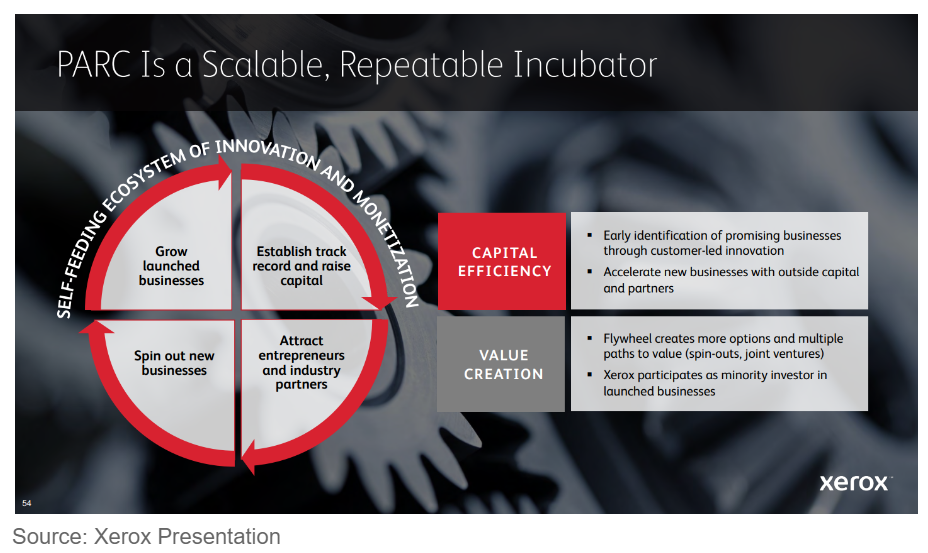

PARC pie-in-the-sky ideas may stay in the research lab and might not get commercialized.

Conclusion

In 1938, Chester Carlson invented xerography, an imaging process. Joseph C. Wilson, credited as the "founder of Xerox", saw the promise of Carlson's invention and, in 1946, signed an agreement to develop it as a commercial product; Xerox was born.

Xerox became a fixture for small and large businesses. No wonder Xerox became part of the business lexicon.

Steve Jobs visited the Xerox PARC facility which resulted in an aha! moment, a graphical user interface. All of us use a graphical user interface every day.

We believe Xerox's old business can continue to provide decent cash flow while other businesses can take off.

As Xerox valuation has declined significantly, another company headed by an alpha male may purchase Xerox to take advantage of low interest rates. Will Carl Icahn agree to sell the company? Yes, if he gets a pretty penny.

We do not engage in day trading so we don’t expect Xerox to double overnight. For investors to realise Xerox's intrinsic value may take some time. How long? 3 months, 6 months, 3 years? We believe at the current price Xerox offers an appetising opportunity for long-term investment, a time horizon of 3-5 years duration.

Disclaimer

We have a beneficial long-term position in the shares of Xerox either through stock ownership, options, or other derivatives. We wrote this article to express our opinions. We are not receiving compensation from any individual or entity for it.

If the management makes mistakes, the economy tanks, competitions give away printers at no charge, Carl Icahn loses interest in Xerox, or for any other reason, Xerox’s stock price can decline dramatically. We do not guarantee that Xerox stock price will increase but we say clearly and loudly that as we believe that Xerox is undervalued, we invested our own money in Xerox.

You should not treat any opinion expressed in this article as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of our opinion. This is not investment advice. Before you invest in anything you might possibly read in our articles or those of the other people offering investment advice online, do your own research to verify the soundness of what you might have read. Please consult your investment advisor before making any decisions.

We do not guarantee you that the stock price will result in a profit. You know that you can lose money on any investment, including this one. We express our opinion via this article, which does not amount to any kind of financial advice. After reading the article, you decide for yourself what steps to take. Please do not blame us if you lose money. By the way, we change our opinions quite often, and when we change our opinion, we are not obliged to inform you. Please carefully review our full disclosure here.

Comments